Selling House During Chapter 13 Bankruptcy Texas: What You Must Know First

Selling house during Chapter 13 bankruptcy Texas is possible, but it requires court and trustee approval before you can close. Here is a quick overview of what the process involves:

- You must file a Motion to Sell with the bankruptcy court

- Your trustee must review and approve the proposed sale

- Creditors receive a notice period and can raise objections

- Sale proceeds go toward your repayment plan first

- A cash buyer with no financing contingencies gives you the fastest, cleanest path to close

Understanding each of these steps can mean the difference between a smooth exit from bankruptcy and a dismissed case. This guide walks you through every stage when selling your home during bankruptcy.

Greenlight Offer is not a bankruptcy attorney. This article provides general information only. Consult a licensed bankruptcy attorney in Texas for advice on your specific case.

Chapter 7 vs. Chapter 13 Bankruptcy: How Each Affects Your Home

Before diving into the sale process, it helps to understand how Chapter 13 differs from Chapter 7, because the rules around selling your home are completely different under each chapter.

Chapter 7 (Liquidation) is often called a “fresh start” bankruptcy. A court-appointed trustee takes control of your non-exempt assets and liquidates them to pay creditors. Under Texas’s generous homestead exemption, most primary residences are protected. If your home is exempt, the trustee typically abandons it, and you regain control to sell once the case closes, usually three to six months after filing.

Chapter 13 (Wage Earner’s Plan) works differently. You keep your home and propose a structured repayment plan lasting three to five years. However, because the court oversees your assets throughout that period, you cannot simply decide to sell whenever you want. You need explicit permission from both the trustee and the bankruptcy judge.

Pro Tip: Texas personal bankruptcy filings rose by over 11% from March 2024 to March 2025, according to court records. If you are among the thousands navigating a Chapter 13 case right now, you are not alone, and selling your home during this period is a well-worn legal path, not an unusual request.

Can You Sell Your House While in Chapter 13 Bankruptcy?

Yes, you can sell your house while in an active Chapter 13 bankruptcy case in Texas. However, the sale cannot proceed without court approval; this is not optional or a formality. As noted by the Chapter 13 trustee office for the Southern District of Texas, you generally cannot sell, refinance, gift, or dispose of any property during a Chapter 13 case without a bankruptcy judge’s approval. That includes your home, your car, and even personal belongings of significant value.

The good news: courts frequently approve home sales during Chapter 13, because selling often accelerates repayment to creditors, which is precisely what Chapter 13 is designed to accomplish.

There is no minimum waiting period before you can request to sell. The motion can be filed at any point during your active case.

The Trustee Approval Process: What’s Required and How Long It Takes

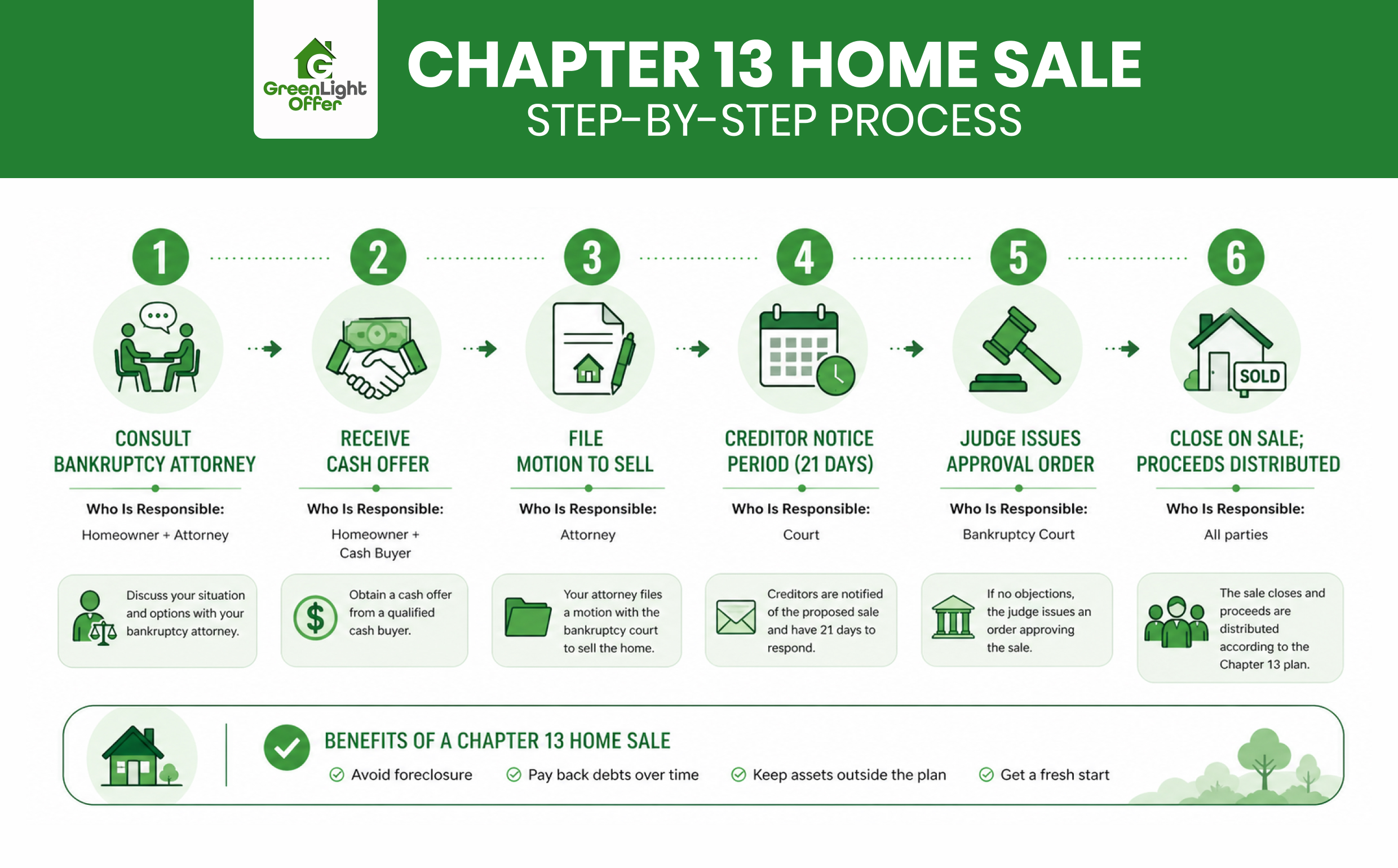

The trustee approval process follows a specific sequence. Skipping any step risks having the sale rejected or the case dismissed.

Step 1: Consult your bankruptcy attorney. Your attorney must evaluate how the sale will affect your repayment plan before any motion is filed. If you have not retained counsel, now is the time.

Step 2: File a Motion to Sell. Your attorney files a motion with the bankruptcy court that outlines the proposed buyer, the sale price, any outstanding mortgage balance, estimated closing costs, and the proposed closing date.

Step 3: Notify creditors. All creditors receive formal notice of the proposed sale and have an opportunity to object. This notice period typically runs 21 days in most Texas district courts, though local rules may vary.

Step 4: Await court approval. If no creditors object, or if objections are resolved, the bankruptcy judge issues an order approving the sale. Once that order is in hand, closing can proceed.

Total timeline: From filing the motion to closing, expect four to six months in most Texas cases. If you work with a cash buyer who has experience in bankruptcy sales, the non-legal portions of the transaction move quickly; the timeline is largely driven by the court calendar.

Pro Tip: File the motion to sell as early as possible in the process. Delays often happen when sellers wait until they are already under contract before contacting their attorney. Start the legal process first, then finalize the purchase agreement.

The Automatic Stay: How It Affects Buyers and the Sale Timeline

When you filed for Chapter 13, an automatic stay went into effect immediately. This legal protection halted all collection actions, including foreclosure proceedings, against you. However, it also has implications for buyers.

A traditional buyer using mortgage financing must wait for the court’s approval order before the lender will proceed to closing. Lenders are generally unwilling to fund a transaction that is still legally in the hands of a bankruptcy estate. This means conventional financed buyers introduce significant uncertainty into the timeline.

The automatic stay can also be lifted by a creditor or the trustee if the sale stalls or if the case is mismanaged, which would remove your protection from foreclosure and other collection actions.

This is one of the primary reasons cash buyers are by far the most practical option in Chapter 13 situations. They do not need lender approval, have no financing contingency, and can close on a flexible timeline that accommodates the court’s schedule.

Why Cash Buyers Are Often the Only Realistic Option in Bankruptcy Situations

When selling a home during a Chapter 13 case, the intersection of court timelines, creditor notices, and automatic stay requirements creates a situation that most traditional buyers simply cannot accommodate.

Consider the practical obstacles with a financed buyer:

- Their lender may refuse to underwrite a purchase involving a bankruptcy estate

- The appraisal and underwriting process creates timing conflicts with the court’s approval window

- Any delay on the buyer’s side can result in motions expiring, requiring refiling

Cash buyers, by contrast, bring several structural advantages to a bankruptcy sale:

- No financing contingency means no risk of a failed transaction

- Flexible closing dates accommodate court scheduling without penalty

- Experienced cash buyers understand the motion process and work directly with attorneys

- As-is purchase terms eliminate repair negotiations, inspection delays, and re-inspection requirements

This is why homeowners facing a sale during Chapter 13 often find that a direct cash offer is not just convenient — it is the only realistic way to complete the transaction within the required legal framework.

Net Proceeds in a Chapter 13 Sale: How Are They Distributed?

Understanding how sale proceeds are distributed is critical before you decide to sell. The distribution order is set by the bankruptcy court and follows a structured priority system:

- Mortgage payoff: Your lender is paid first from the sale proceeds

- Closing costs: Title fees, transfer taxes, and related expenses

- Trustee fee: The Chapter 13 trustee typically receives 3–5% of the proceeds they administer

- Creditor repayment: Non-exempt proceeds go toward satisfying your repayment plan obligations

- Homestead exemption: Under Texas law, you may be entitled to keep a portion of the proceeds protected under the homestead exemption

Texas has some of the most generous homestead protections in the country. However, there is a 40-month rule that limits full exemption protection for those who have recently moved to Texas before filing. Your bankruptcy attorney can clarify exactly how much equity you are entitled to retain, given your specific case timeline.

If the sale generates enough proceeds to pay off all remaining creditors in full, the court may allow you to exit Chapter 13 ahead of schedule — sometimes months or years before your original plan’s end date.

Working With Your Bankruptcy Attorney + Greenlight Offer Together

One of the most common mistakes homeowners make in this situation is treating the legal process and the real estate process as separate. They are not. The most successful transactions happen when your bankruptcy attorney and your cash buyer are working in parallel, not in sequence.

Greenlight Offer has worked alongside bankruptcy attorneys in the Houston area and across Texas to facilitate Chapter 13 home sales. Because cash sales involve no lender, no appraisal contingency, and no drawn-out closing timelines, they align naturally with the constraints the court imposes. The team at Greenlight Offer understands the documentation the court requires and can work with your attorney to structure the transaction correctly from day one.

The process is straightforward: you contact Greenlight Offer for a no-obligation cash offer, share that offer with your bankruptcy attorney, and your attorney incorporates the sale into the Motion to Sell. Once the court approves the motion, closing follows quickly, on a date that fits your legal schedule, not the other way around.

Greenlight Offer has served Houston-area homeowners since 2016, with a 4.7-star Google rating backed by verified reviews. There are no commissions, no repair requirements, and no fees deducted from your offer. You receive a cash offer within 24 hours and choose your own closing date.

Frequently Asked Questions About Selling House During Chapter 13 Bankruptcy Texas

Does the trustee have to approve a home sale in Chapter 13?

Yes. You must file a Motion to Sell and receive approval from both the Chapter 13 trustee and the bankruptcy judge before any sale can close. Selling without approval risks case dismissal.

How long does it take to get court approval to sell a house in Chapter 13?

Most Texas courts take four to six weeks from the motion filing date to issue an approval order, assuming no creditor objections. Total time from start to close is typically four to six months.

Will I receive any money from the sale of my home?

Possibly. Proceeds first pay the mortgage, closing costs, and trustee fees. Remaining funds go toward your repayment plan. If you have Texas homestead-exempt equity, you may keep that protected portion.

Can selling my house end my Chapter 13 case early?

Yes. If proceeds satisfy all remaining creditor obligations in full, the court can grant an early discharge and close your case ahead of the original three-to-five-year schedule.

Why can’t I just list my house with a real estate agent during Chapter 13?

You can involve an agent, but the sale still requires court approval regardless of how it is marketed. Additionally, agents’ commissions reduce net proceeds available to creditors, which may complicate trustee approval. Cash buyers typically result in fewer deductions and a simpler approval motion.

Selling House During Chapter 13 Bankruptcy Texas: Your Path Forward

Selling house during Chapter 13 bankruptcy Texas is a legally structured process, but it is entirely achievable with the right team in place. The steps are clear: get legal counsel, file the motion, notify creditors, obtain court approval, and close. A cash buyer removes the variables that most commonly derail this process.

If you are currently in a Chapter 13 case and considering a home sale, the smartest first move is a conversation with your bankruptcy attorney, followed immediately by a call to Greenlight Offer. Getting a cash offer costs nothing and gives your attorney the concrete numbers needed to build a strong Motion to Sell.

Greenlight Offer has no commissions, requires no repairs, and has helped Houston-area homeowners navigate distressed property sales since 2016. You can reach the team at (713) 588-5824 or request your offer at greenlightoffer.com.