Capital Gains Tax on Inherited Property in Texas: What You Need to Know

Capital gains tax on inherited property in Texas is often far lower than most heirs expect — and in many cases, you may owe nothing at all. If you recently inherited a home and are weighing your options, here is what the tax picture actually looks like:

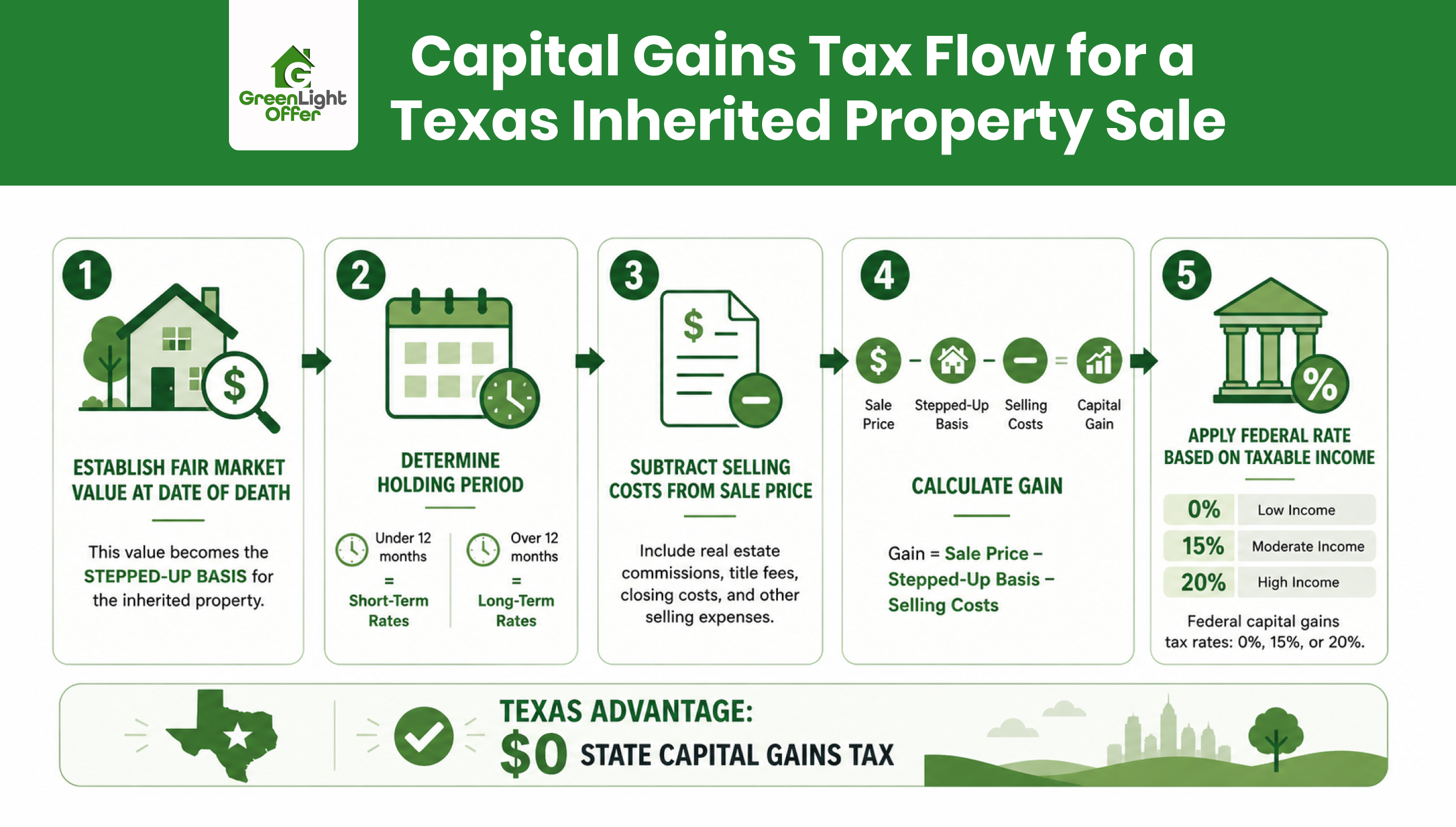

- Texas has no state income tax, estate tax, or inheritance tax

- Federal capital gains tax only applies to appreciation after the date of death

- The stepped-up basis rule resets your cost basis to the home’s value when you inherited it

- Selling quickly, converting to a primary residence, or working with a cash buyer each carry different tax outcomes

- A CPA can help you determine your exact liability before you close

Understanding these rules now protects you from unnecessary surprises at closing.

Does Texas Have an Estate Tax or Inheritance Tax?

Texas does not impose a state estate tax or inheritance tax. This sets Texas apart from states like Maryland, Pennsylvania, and New Jersey, which tax certain heirs directly.

When someone passes away in Texas and leaves property to a beneficiary, the state takes no cut of that transfer. The heir receives the asset without owing anything to Texas.

However, federal rules still apply. The federal estate tax only affects very large estates. For 2026, the federal exemption is approximately $15 million per individual, meaning estates below that threshold owe no federal estate tax either.

For the vast majority of Texas families, neither state nor federal estate taxes factor into an inherited home sale. The tax that most heirs encounter — capital gains — operates entirely separately.

Pro Tip: The federal estate tax is paid by the estate itself before assets are distributed. If you are an heir receiving a home, you are not responsible for any estate taxes owed. Confirm with the estate executor that all obligations were settled before you proceed with a sale.

What Is the Stepped-Up Basis Rule and Why Does It Matter for Inherited Homes?

The stepped-up basis rule is the single most important tax concept for anyone inheriting real estate. Under this IRS rule, your cost basis in an inherited property is reset to the home’s fair market value on the date the original owner died, not what they originally paid for it.

Here is why that matters in practice. Suppose your parent bought a Houston home for $120,000 in 1995. By the time they passed, that home was worth $380,000. Without the stepped-up basis, you would potentially owe capital gains tax on up to $260,000 of appreciation. With the stepped-up basis, your cost basis becomes $380,000. If you sell at that same price, your taxable gain is zero.

This rule applies automatically in Texas as part of the federal estate settlement process. You do not need to take extra steps to claim it. However, you do need an accurate appraisal of the property’s value on the date of death. That appraisal becomes the foundation of all future tax calculations.

Additionally, Texas is a community property state. When one spouse dies, both halves of the community property receive a stepped-up basis, a double step-up. This benefit is unique to community property states and can substantially reduce tax liability for surviving spouses who later sell.

Pro Tip: Order a professional appraisal as close to the date of death as possible. Appraisals completed months or years later are harder to defend with the IRS. This document becomes critical if you hold the property and sell it years down the road.

How Capital Gains Tax Is Calculated on an Inherited Home Sale

Capital gains tax on inherited property is calculated on the difference between your sale price and your stepped-up basis. There are two rates to understand: short-term and long-term.

Short-term capital gains apply when you sell within 12 months of inheriting. These gains are taxed at ordinary income rates, which can reach as high as 37% depending on your tax bracket. This is the less favorable scenario.

Long-term capital gains apply when you hold the property for more than 12 months before selling. For 2026, the federal long-term rates are:

| Taxable Income (Single Filer) | Capital Gains Rate |

|---|---|

| Up to $48,350 | 0% |

| $48,351 – $533,400 | 15% |

| Over $533,400 | 20% |

For married couples filing jointly, the 0% threshold rises to approximately $96,700 in taxable income.

Because Texas has no state income tax, these federal rates represent your total capital gains obligation. There is no additional Texas layer.

The calculation itself is straightforward:

Capital Gain = Sale Price – Stepped-Up Basis – Selling Costs

Allowable selling costs include agent commissions, closing costs, and any capital improvements you made to the property after inheriting it. These deductions reduce your taxable gain directly.

Example Calculation: Inherited Houston Home — Tax Impact Scenarios

The following examples illustrate how the tax math works for a typical inherited Houston property.

Base scenario: You inherit a home appraised at $320,000 on the date of death. Your stepped-up basis is $320,000.

Scenario A — Sell immediately at market value Sale price: $325,000 Stepped-up basis: $320,000 Selling costs: $12,000 Net taxable gain: ($325,000 – $320,000 – $12,000) = $0 (net loss, no tax owed)

Scenario B — Hold 18 months, sell after appreciation Sale price: $360,000 Stepped-up basis: $320,000 Selling costs: $15,000 Net taxable gain: $25,000 Tax at 15% long-term rate: $3,750

Scenario C — Sell within 6 months at higher price (short-term) Sale price: $370,000 Stepped-up basis: $320,000 Selling costs: $15,000 Net taxable gain: $35,000 Tax at 22% ordinary income rate: $7,700

These scenarios demonstrate a key point: timing and selling costs have a real impact on what you owe. Selling quickly near the stepped-up value, or using a cash buyer with minimal fees, often results in the lowest tax bill.

3 Ways to Minimize or Avoid Capital Gains Tax on an Inherited Home

There are several legitimate strategies to reduce or eliminate capital gains tax on an inherited home. The right choice depends on how quickly you need to sell and what you plan to do with the property.

1. Sell Quickly at or Near the Stepped-Up Value

The most straightforward strategy is selling the property as soon as possible after inheriting it. Because your cost basis resets to the date-of-death value, a quick sale at that same market price produces little to no taxable gain. Any selling costs you incur further reduce the taxable amount.

This approach works especially well for heirs who do not want to manage the property long-term. A direct cash sale to a home buyer eliminates agent commissions — typically 5–6% of the sale price — which means more of the proceeds stay in your pocket and your taxable gain shrinks accordingly.

2. Convert the Property to Your Primary Residence

If you move into the inherited home and use it as your primary residence for at least two of the next five years, you may qualify for the federal primary residence exclusion. Under current IRS rules, single filers can exclude up to $250,000 in capital gains from the sale; married couples filing jointly can exclude up to $500,000.

This strategy makes sense when the property is in good condition, located where you want to live, and you have time to meet the residency requirement. However, it involves ongoing costs — property taxes, insurance, maintenance — that should factor into your decision.

3. Use a 1031 Exchange to Defer Gains

If you plan to reinvest the sale proceeds into another investment property, a 1031 exchange allows you to defer capital gains tax indefinitely by rolling gains into a replacement property. This strategy requires strict timing: you must identify the replacement property within 45 days of the sale and close within 180 days.

A qualified intermediary must hold the funds during the exchange. This is not a do-it-yourself process — work with a tax professional experienced in 1031 exchanges before proceeding.

Each of these paths has tax and practical trade-offs. Consulting a CPA before committing to any strategy is the most reliable way to protect your financial outcome.

Selling to a Cash Buyer vs. Waiting — Tax Timing Considerations

Many heirs assume waiting to sell produces a better financial outcome. Sometimes it does. However, holding an inherited property has real carrying costs that reduce net proceeds over time.

Carrying costs to consider while holding:

- Property taxes (the prior owner’s homestead exemption does not transfer automatically)

- Homeowner’s insurance

- Maintenance and repairs

- Any existing mortgage payments

- Possible HOA fees

Furthermore, if you sell within 12 months of inheriting, any gain is taxed at short-term rates. Consequently, holding for just over 12 months to qualify for long-term rates can reduce your tax bill significantly — particularly if the property has appreciated.

On the other hand, a fast cash sale locks in a gain calculation close to the stepped-up basis. This often means minimal or zero tax owed, especially when selling costs offset any modest appreciation. For heirs dealing with probate property in Houston, speed frequently outweighs the marginal benefit of waiting for additional appreciation.

The key calculation is: what do you net after holding costs, selling costs, and taxes — not simply the sale price on the listing sheet.

When Should You Consult a Tax Professional or CPA?

Taxes on inherited property are one area where professional guidance pays for itself. You should consult a CPA or tax attorney before selling if any of the following apply:

- The property has appreciated significantly since the date of death

- You are considering a 1031 exchange or installment sale

- Multiple heirs are involved and you are splitting proceeds

- The estate involves community property or trust structures

- You are unsure whether the stepped-up basis was correctly documented

- You inherited property from someone in another state

A CPA can also help you determine whether any deductions — repairs, depreciation if rented, or capital improvements — apply to your specific situation. The tax rules around inherited property are favorable in Texas, but getting the documentation right matters as much as understanding the rates.

Why Texas Heirs Choose Greenlight Offer to Sell Inherited Homes

Selling an inherited home involves more than finding a buyer. Heirs often face probate timelines, deferred maintenance, and the emotional weight of parting with a family property. Greenlight Offer was built specifically to handle these situations.

Since 2016, Greenlight Offer has helped Houston-area homeowners sell inherited and probate properties quickly, without the friction of traditional listings. Here is what that means in practice for heirs navigating a sale:

No repairs required. Greenlight Offer buys properties as-is. You are not responsible for fixing deferred maintenance, clearing out belongings, or bringing the home up to listing condition.

No agent commissions or hidden fees. Traditional sales typically cost 5–6% in commissions alone. With Greenlight Offer, the cash offer is what you take home — zero closing costs on your side.

Closing on your timeline. The company can close in as little as 14 days or work around your probate or estate administration schedule. This flexibility matters when multiple heirs or an executor are involved.

A cash offer in 24 hours. Once you submit your property details, Greenlight Offer delivers a no-obligation offer within 24 hours. There is no pressure to accept.

For heirs who want to minimize capital gains exposure by selling close to the stepped-up value, a fast cash sale often achieves exactly that — while eliminating the holding costs that erode net proceeds over time.

Greenlight Offer serves Houston, Conroe, Baytown, Pearland, The Woodlands, Katy, League City, and surrounding areas.

Frequently Asked Questions About Capital Gains Tax on Inherited Property Texas

Do I owe capital gains tax the moment I inherit a Texas home?

No. Capital gains tax only applies when you sell the property. Inheriting itself is not a taxable event under federal or Texas law.

What if my inherited home has declined in value since the owner died?

If you sell for less than the stepped-up basis, you have a capital loss. Losses on inherited personal-use property are generally not deductible, but a CPA can advise on your specific situation.

How does the stepped-up basis apply if multiple heirs inherit the property?

Each heir’s share receives the same stepped-up basis proportionally. All heirs must typically agree to sell, or one heir can buy out the others at the stepped-up value.

Can I deduct the costs of fixing up the inherited home before selling?

Capital improvements you make after inheriting can increase your cost basis and reduce taxable gain. Routine repairs, however, are generally not deductible against capital gains.

Does living in the inherited home before selling affect my tax liability?

Yes. If you occupy it as your primary residence for two of the five years before selling, you may exclude up to $250,000 ($500,000 for married couples) in gains under the IRS primary residence exclusion.

Your Next Step: Understanding Capital Gains Tax on Inherited Property in Texas

Capital gains tax on inherited property in Texas is manageable — especially with the stepped-up basis working in your favor. The key facts: Texas charges no state capital gains tax, federal rates depend on your income and holding period, and selling quickly near the inherited value often means owing little or nothing.

For heirs who want certainty and speed, a direct cash sale eliminates commissions, repairs, and the carrying costs of an extended listing. Greenlight Offer has helped hundreds of Houston-area families navigate exactly this situation since 2016.