Understanding the Fast Cash Home Buying Process

Buy homes fast cash companies are real estate investors and businesses that purchase properties directly from homeowners using their own funds, eliminating the need for buyer financing and traditional mortgage approvals. Here’s what you need to know:

Quick Answer:

- Who They Are: Real estate investors, iBuyers, and cash buying companies

- Timeline: Close in 10-14 days vs. 30-45 days for traditional sales

- Payment: 50-95% of market value depending on buyer type and property condition

- Benefits: No repairs needed, no agent commissions, flexible closing dates

- Best For: Foreclosure situations, inherited properties, major repairs needed, quick relocations

The cash home buying industry has exploded in recent years. According to the National Association of Realtors, 29% of home sales in January 2025 were all-cash transactions. That’s nearly 1 in 3 homes sold without any financing involved.

But what do these companies actually do with the homes they buy? How do they make money? And most importantly – is selling to them the right choice for your situation?

The answers aren’t always straightforward. Some cash buyers are legitimate investors who renovate and resell properties. Others are large tech companies using algorithms to flip homes at scale. And unfortunately, some are scammers looking to take advantage of desperate homeowners.

What Does It Really Mean to Sell a House for Cash?

When companies say they’ll buy homes fast cash, they’re talking about using their own money instead of getting a loan from a bank. It’s really that simple – but the impact on your selling experience is huge.

Think about it this way: in a traditional sale, your buyer has to jump through hoops with a mortgage lender. They need credit approval, income verification, an appraisal, and about a dozen other steps that can take weeks or even months. Any one of these steps can derail the entire deal.

With a cash buyer, none of that happens. They show proof of funds – basically bank statements proving they have the money sitting in their account. Then you both sign papers at a title company, just like any other real estate transaction, and you get paid. No waiting around wondering if their loan will get approved.

The speed difference is remarkable. While traditional sales average 42 days from contract to closing, buy homes fast cash transactions often close in just 10-14 days. According to the latest data from the National Association of Realtors, 29% of all home sales are now cash transactions. That means nearly 1 in 3 sellers are choosing this route.

But here’s what really matters: it’s not just about speed. It’s about certainty and peace of mind during what’s often a stressful time in your life.

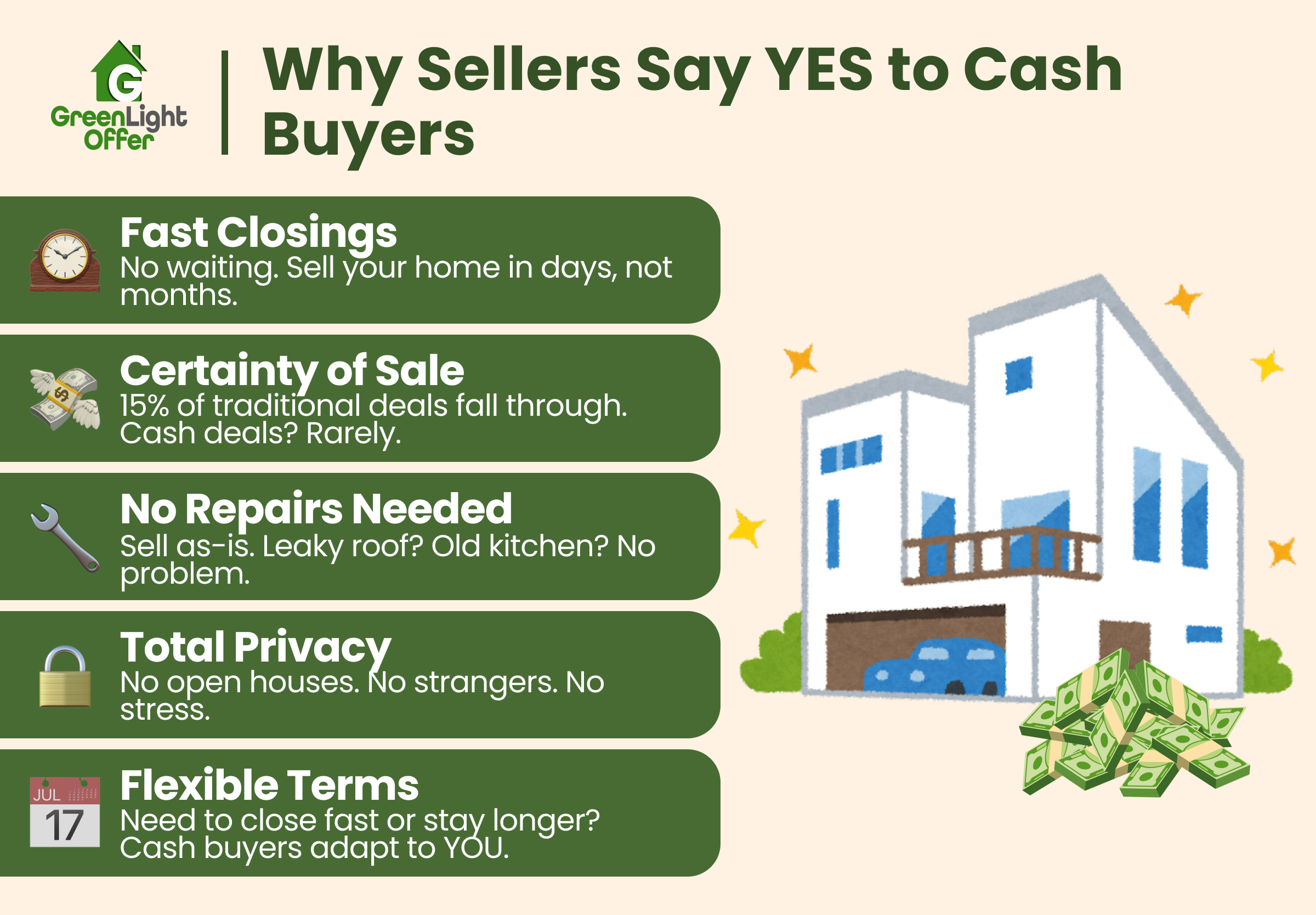

Top Reasons Sellers Choose Cash

Speed is obvious, but there’s so much more to the story. Let me share what I’ve learned from working with thousands of Houston homeowners over the years.

Certainty is probably the biggest advantage people don’t expect. Traditional sales fall through about 15% of the time – usually because of financing problems or appraisal issues. When you’re counting on that sale to happen, a last-minute cancellation can be devastating. Cash sales rarely fall through once the contract is signed.

No repairs needed is a game-changer for many sellers. Most cash buyers purchase homes “as-is,” which means exactly what it sounds like. That leaky roof? The outdated kitchen? The carpet your dog had an accident on five years ago? None of it matters. They’ll handle everything after they buy it.

Privacy matters more than people realize. There are no open houses, no strangers walking through your bedrooms, no agents showing up at inconvenient times. Many cash buyers can make offers based on photos or a quick walkthrough, respecting your space during what might already be a difficult situation.

Unique situations get handled with flexibility that traditional buyers simply can’t match. Need to close in a week because of a job transfer? Want to stay in the house for two months while you find your next place? Cash buyers often accommodate timing requests that would make conventional buyers run for the hills.

Situations Best Suited for a Cash Sale

Cash sales aren’t right for everyone, but they’re perfect for certain situations. I’ve seen them be absolute lifesavers for families dealing with tough circumstances.

Pre-foreclosure situations are where cash buyers really shine. When you’re facing foreclosure, every day counts. Cash buyers can often close before the auction date, helping you avoid the credit damage and potentially saving some of your equity. It’s not a perfect solution, but it’s often the best option available.

Inheritance can turn into a nightmare, especially if you live far away from the property. I’ve worked with families trying to deal with a parent’s house from three states away. Cash buyers handle everything – from clearing out belongings to dealing with title issues – turning a months-long headache into a simple transaction.

Vacant properties are money pits. You’re paying utilities, insurance, and property taxes on a house nobody’s living in. Plus, empty houses attract problems – vandalism, break-ins, or squatters. Cash buyers eliminate all these ongoing costs and risks quickly.

Major repairs can make traditional sales impossible. When your house needs a new roof, foundation work, or extensive renovations, the cost to get it market-ready might be more than you’d gain in sale price. Cash buyers factor these repairs into their offers, essentially buying your problems along with your house.

Landlord burnout is real. After years of dealing with problem tenants, 3 AM maintenance calls, and changing rental regulations, many property owners just want out. Cash buyers often specialize in rental properties and can close even with tenants still living there.

The bottom line? If you need to sell quickly, can’t afford repairs, or just want a simple transaction without the usual real estate drama, cash buyers might be exactly what you’re looking for.

How to “Buy Homes Fast Cash”: A Step-By-Step Playbook

Selling your home to a buy homes fast cash company is surprisingly simple – much easier than the traditional real estate maze most homeowners expect. The entire process typically wraps up in just 10-14 days, compared to the 30-60 day marathon of conventional sales.

Here’s exactly what happens from your first phone call to walking away with cash in hand:

The First 48 Hours start with you reaching out, usually through a simple online form or quick phone call. You’ll share basic details about your property – the address, rough square footage, current condition, and when you need to close. Most reputable cash buyers can give you a preliminary offer within hours, not weeks.

Days 3-7 involve the property evaluation. This isn’t the stressful, white-glove inspection you’d face with traditional buyers. Many cash buyers can work with photos and videos for a virtual walk-through, especially if you’re not local or prefer minimal disruption. They’re simply confirming your home’s condition matches what you’ve described.

The Final Week moves fast. Once you accept their offer, the buyer handles the heavy lifting – ordering the title search, coordinating with the title company, and preparing all closing documents. You’ll typically sign everything and receive payment on the same closing day.

The beauty of this timeline is its predictability. While traditional sales can stretch for months or fall through at the last minute, cash transactions rarely hit major snags once both parties sign the contract.

For more detailed guidance on navigating this process, check out our comprehensive guide on How to Sell a House Quickly.

Getting Ready to Buy Homes Fast Cash

Even though cash sales are refreshingly simple, a little preparation goes a long way toward ensuring everything runs smoothly.

Start by collecting your important documents. You’ll need your property deed, current mortgage statements showing exactly what you owe, recent property tax bills, and any homeowners association information. If you happen to have old surveys, inspection reports, or receipts from major improvements, these can be helpful – but don’t stress if you can’t find them.

Next, get your exact mortgage payoff amount from your lender. This number changes daily because of interest, so request a payoff statement that’s good for at least 30 days. Don’t forget to ask about any prepayment penalties that might apply.

Take a moment to think about anylienson your property beyond your main mortgage. This could include tax liens, contractor liens from unpaid work, or HOA liens. Knowing about these upfront prevents unpleasant surprises at closing.

Finally, prepare any required property disclosures. Even though cash buyers purchase homes “as-is,” you’re still legally required to share known problems or defects. Most buyers appreciate honesty – it builds trust and keeps everyone protected.

Accepting the “Buy Homes Fast Cash” Offer

When that cash offer lands in your inbox, take a breath and review it carefully. Speed doesn’t mean you should skip the important details.

Look for earnest money in the contract. Serious buyers put down $1,000 to $5,000 to show they’re committed. This money goes into a secure escrow account and gets applied to your final sale price at closing.

Even though these deals move quickly, contract review matters. Read through all the terms, looking for any contingencies, repair credits, or unusual conditions. If something doesn’t make sense, don’t hesitate to ask questions or have an attorney take a look.

Before you sign anything, make sure the buyer provides proof of funds – typically a recent bank statement or letter from their financial institution showing they actually have the money available. This simple step protects you from buyers who are all talk and no cash.

Legitimate cash buyers understand you might want attorney advice before proceeding. If a buyer pressures you to sign immediately without any review time, that’s often a red flag worth heeding.

The Upside & Downside: Benefits vs Risks

I wish I could tell you that selling to buy homes fast cash companies is perfect for everyone, but that wouldn’t be honest. Like any major financial decision, there are real advantages and genuine drawbacks to consider.

The speed alone can be life-changing. When you’re facing foreclosure or need to relocate for a job in two weeks, closing in 10-14 days instead of waiting months can literally save your financial future. I’ve seen families avoid bankruptcy simply because they could access their home equity quickly.

Convenience is another huge factor that people underestimate until they experience it. No staging your home to perfection, no keeping it spotless for surprise showings, no strangers wandering through your bedrooms every weekend. You can sell your house while still living your normal life.

The certainty factor eliminates the emotional rollercoaster of traditional sales. You won’t get that devastating call three days before closing saying the buyer’s financing fell through. Once you shake hands with a cash buyer, you can actually count on the deal happening.

Cost savings extend beyond the obvious elimination of real estate agent commissions, which typically run 6% of your sale price. You’ll also save weeks or months of holding costs – mortgage payments, insurance, utilities, and maintenance. For a $200,000 home, those holding costs can easily exceed $2,000 per month.

But let’s talk about the elephant in the room: you’ll typically receive less money than if you sold through traditional methods. This isn’t a secret that cash buyers are hiding – it’s the trade-off for speed and convenience.

Limited negotiation can be frustrating if you’re used to the back-and-forth of traditional real estate deals. Many cash buyers present their best offer upfront with little room for haggling. They’ve done their math and know their margins.

The due diligence burden falls entirely on you. Unlike working with a licensed real estate agent who vets buyers, you need to verify that your cash buyer is legitimate, has the funds they claim, and will actually close on time.

Who Covers Fees & Closing Costs?

Here’s where cash sales often surprise sellers in a good way. Most reputable buy homes fast cash companies cover the majority of closing costs that would normally come out of your pocket.

Buyer-paid costs typically include title insurance and search fees, settlement or escrow fees, recording fees, and transfer taxes. Many cash buyers also cover attorney fees if your state requires legal representation at closing.

You’ll still be responsible for outstanding property taxes, any HOA fees or special assessments, and of course, paying off your existing mortgage including any prepayment penalties. These aren’t really “closing costs” – they’re existing obligations that follow the property.

The beauty is in the simplicity. When a cash buyer says “no fees to you,” they usually mean it. Always ask for a net sheet that shows exactly what you’ll receive after all costs and fees. This transparency helps you compare offers fairly.

For more detailed information about maximizing your cash offer, visit our page on Instant Cash Offer for House.

How Much Below Market Should You Expect?

This is the question that keeps sellers up at night, and honestly, the answer varies more than most people realize.

Traditional real estate investors typically offer between 50-70% of a property’s after-repair value, then subtract their estimated repair costs. This might sound low, but remember – they’re taking on all the risk of renovations, market changes, and holding costs while the work gets done.

iBuyer companies often present offers in the 85-95% range of current market value, which sounds much better until you read the fine print. They typically charge service fees of 5-6%, plus additional fees for repairs or improvements, bringing your actual net proceeds much closer to traditional investor offers.

Property condition dramatically impacts offers. A move-in ready home in a desirable neighborhood might fetch 80-90% of market value, while a property needing major repairs could see offers at 50-60% of its potential value.

Local market conditions matter too. In hot markets where inventory is scarce, cash buyers compete more aggressively. In slower markets with plenty of options, they can afford to be more selective with their pricing.

The smartest approach? Get multiple offers. Even if they’re all below retail market value, you might be surprised by the variation between different buyers. That difference could mean thousands of dollars in your pocket.

Who Actually Buys Homes Fast for Cash? Investors, iBuyers & More

When you’re exploring options to buy homes fast cash, you’ll encounter several different types of buyers, each with their own motivations and business models. Understanding who’s behind these cash offers helps you make smarter decisions about which buyer might be the best fit for your situation.

House flippers (active in the real estate flipping niche) are probably the most well-known cash buyers. These investors specialize in purchasing distressed properties, renovating them quickly, and reselling them for profit. They’re particularly interested in homes that need cosmetic updates or moderate repairs in desirable neighborhoods. If your house has good bones but needs a kitchen update or fresh paint throughout, flippers might be your most competitive buyers.

Buy-and-hold landlords represent another major category of cash buyers. These investors are building rental property portfolios and often pay cash to move quickly on properties with good cash flow potential. They’re typically less concerned about cosmetic issues since they’re planning to rent the property rather than flip it immediately. If your home is in a rental-friendly area, these investors might offer competitive prices even if the property isn’t picture-perfect.

The newest players in the cash buying space are iBuyers – technology companies that use sophisticated algorithms to make instant offers on homes. These companies typically focus on newer homes in good condition and can provide offers within minutes of receiving your property information. They’ve streamlined the entire process but usually charge service fees for the convenience they provide.

Wholesalers operate differently from other cash buyers. They get properties under contract at below-market prices, then assign those contracts to other investors for a fee. Since they need room for both their assignment fee and the end buyer’s profit margin, wholesalers often make the lowest offers you’ll receive. However, they can sometimes close very quickly if they already have end buyers lined up.

Estate buyers and mom-and-pop investors round out the landscape. Estate buyers specialize in inherited properties, probate sales, and complex family situations. They understand the unique challenges these transactions present and often provide additional services like property cleanouts or dealing with multiple heirs. Local mom-and-pop investors might not have the marketing budgets of larger companies, but they often bring decades of experience and can handle unusual situations that other buyers avoid.

Investor Math 101

If you’ve ever wondered how investors come up with their offer prices, understanding their basic math helps you evaluate whether their numbers are reasonable.

Most investors start with the After Repair Value (ARV) – what your property will be worth after all improvements are complete. They determine this by looking at comparable sales of similar homes in move-in ready condition in your neighborhood.

Many investors then apply what’s called the 70% rule. This rule of thumb says they’ll pay no more than 70% of the ARV minus their estimated repair costs. So if your home will be worth $200,000 after repairs, and those repairs will cost $30,000, an investor using this formula would offer no more than $110,000 ($200,000 x 70% = $140,000 minus $30,000 in repairs).

The repair budget isn’t just guesswork. Professional investors typically get contractor estimates for all needed work, then add a contingency buffer for unexpected problems that always seem to pop up during renovations.

Finally, investors need a profit margin to make the risk and work worthwhile. After all, they’re investing their time, money, and expertise, and taking on the risk that something could go wrong. Typical profit margins range from 15-25% of the final sale price, which might seem high until you consider all the work and risk involved in renovating and reselling a property.

iBuyers vs Local Investors

The choice between iBuyers and local investors often comes down to your priorities and your property’s characteristics.

iBuyers excel at speed and convenience. Their automated valuation models can provide offers within minutes, and their standardized processes eliminate much of the uncertainty from selling. They often offer higher initial prices but typically charge service fees that can range from 5-6% of the sale price. They also have strict property criteria – they prefer newer homes in good condition in suburban neighborhoods.

Local investors bring market knowledge and flexibility that algorithms can’t match. They can handle unusual properties, complex family situations, or homes that don’t fit standard criteria. Their offers might be lower initially, but they often have fewer fees and more flexibility on timing, repairs, or other terms that matter to you.

The key difference is that iBuyers prioritize convenience and speed, while local investors often provide more personalized service and can work with challenging situations. Neither approach is inherently better – it depends on what matters most in your specific situation.

Staying Safe: Vetting Buyers & Avoiding Scams

Let’s talk about the elephant in the room – not everyone claiming to buy homes fast cash is legitimate. The industry’s rapid growth has unfortunately attracted some bad actors who prey on homeowners in vulnerable situations.

I’ve seen too many stories of sellers who got burned by fake buyers, bait-and-switch tactics, or outright scams. The good news? Legitimate cash buyers are easy to identify once you know what to look for.

Start with their Better Business Bureau rating. Any reputable company should have a solid BBB profile with mostly positive reviews. Don’t just look at the overall rating – read recent complaints to see if there are patterns of problems. If a company has multiple complaints about changing offers at the last minute or failing to close deals, that’s a red flag.

Demand proof of funds before you sign anything. This isn’t negotiable. A legitimate buyer should provide recent bank statements or a letter from their lender showing they actually have the money available. If someone says “trust me” or promises to show proof later, walk away. Real cash buyers understand this request and come prepared.

Ask for references from recent sellers. Most reputable buyers are happy to provide contact information for homeowners they’ve recently worked with. Take the time to call a few references. Ask about their experience – did the buyer stick to their original offer? Did they close on time? Would they work with this buyer again?

Require earnest money held by a neutral third party. Serious buyers put their own money at risk by depositing earnest money with a title company or attorney. This shows they’re committed to the deal and gives you recourse if they back out without cause. If a buyer won’t provide earnest money, they’re probably not serious.

Watch for pressure tactics and unrealistic promises. Legitimate buyers give you time to think and ask questions. Be suspicious of anyone who pressures you to sign immediately, claims their offer expires in hours, or promises prices that seem too good to be true. Real estate transactions involve major financial decisions – rushing you is a red flag.

Never pay upfront fees or wire money to a buyer. This should be obvious, but scammers sometimes ask for “processing fees” or “title fees” upfront. In legitimate transactions, you receive money at closing – you don’t pay it.

For more detailed guidance on choosing reputable cash buyers, check out our resource on the Best Company to Sell House for Cash.

Negotiating & Comparing Multiple Offers

Here’s something many sellers don’t realize – even cash offers aren’t always set in stone. While cash buyers typically present firm offers, you often have more negotiating power than you think.

Request the comparable sales they used. Ask buyers to show you the recent sales data that supports their offer. This transparency helps you understand their pricing methodology and gives you ammunition for negotiations. If their comps seem outdated or from different neighborhoods, point that out.

Get a detailed net sheet from each buyer. Don’t just compare offer prices – look at what you’ll actually receive after all costs and fees. One buyer might offer $10,000 more but charge $8,000 in fees, making the lower offer actually better. A good net sheet shows your gross proceeds, all deductions, and your final check amount.

Consider timing flexibility as a negotiating tool. If you can close faster or slower than requested, use that as leverage. Some buyers will pay more for a quick close, while others might increase their offer if you can wait for their preferred timeline.

Don’t be afraid to counter. Many cash buyers build some negotiating room into their initial offers. The worst they can say is no, and you might be surprised how often they’ll meet you somewhere in the middle.

Evaluate the complete package, not just the price. Consider each buyer’s track record, their flexibility on terms, and how comfortable you feel working with them. Sometimes the highest offer isn’t the best offer if it comes from an unreliable buyer.

Legal & Tax Checkpoints

Before you sign on the dotted line, there are several important legal and tax considerations that could significantly impact your financial outcome.

Ensure a proper title search happens. The buyer should order a comprehensive title search to identify any liens, ownership issues, or other problems that need resolution before closing. This protects both of you and ensures the transaction can actually close.

Consider attorney review for complex situations. While not always required, having an attorney review your contract is smart money for high-value properties, inherited homes, or complicated situations like divorce sales. The few hundred dollars in attorney fees can save you thousands in problems later.

Understand your capital gains tax implications. Depending on how long you’ve owned the property and your profit, you might owe significant taxes on the sale. If you’ve lived in the home as your primary residence for at least two of the last five years, you may qualify for the capital gains exclusion. For investment properties or second homes, the rules are different.

Explore 1031 exchange options for investment properties. If you’re selling a rental property or other investment real estate, you might be able to defer taxes by reinvesting the proceeds in another investment property through a 1031 exchange. This strategy requires specific timing and procedures, so consult a qualified intermediary early in the process.

Consider special estate tax rules for inherited properties. Inherited properties often receive a “stepped-up basis,” which can significantly reduce capital gains taxes. However, there may be timing requirements or other estate-related considerations that affect your sale strategy.

The key is getting professional advice early in the process. A quick consultation with a tax professional or attorney can help you structure the sale in the most tax-efficient way possible.

Frequently Asked Questions about Buy Homes Fast Cash

Let’s tackle the most common questions I hear from homeowners considering a buy homes fast cash sale. These are real concerns from real people, and you deserve straight answers.

Is a real estate agent or lawyer required?

Here’s the good news: you don’t need a real estate agent when selling to a cash buyer. That’s actually one of the biggest advantages – no agent commissions eating into your proceeds, and no waiting around for showings or open houses.

But what about lawyers? It depends on your state. Some states require an attorney to handle the closing, while others allow title companies to manage everything. Even where it’s not required, having an attorney review your contract can give you peace of mind, especially if you’re dealing with a high-value property or a complicated situation.

Think about it this way: if you’re going through a divorce, handling an inheritance, or facing foreclosure, spending a few hundred dollars on legal advice could save you thousands down the road. The cash buyer should be able to recommend attorneys they’ve worked with before.

Can I sell any property condition for cash?

This is where cash buyers really shine. Most cash buyers will purchase homes in any condition – and I mean any condition. Leaky roof? No problem. Foundation issues? They’ll handle it. Kitchen from the 1970s? Perfect.

But let’s be realistic about what “any condition” actually means. Single-family homes, townhomes, and condos in decent neighborhoods are the easiest to sell, regardless of how much work they need. These properties have clear markets and predictable repair costs.

Some situations require more specialized buyers. Homes with major structural problems, environmental hazards, or significant legal issues can still be sold for cash, but you’ll need to find buyers who specifically handle these challenging properties.

The trickiest properties? Think homes with code violations, fire damage, or problem tenants who won’t leave. These can be sold, but expect lower offers and potentially longer timelines while the buyer figures out how to handle the complications.

The most important thing is being completely honest about your property’s condition from the start. I’ve seen deals fall apart because sellers tried to hide problems, thinking they’d get a better offer. Trust me – the buyer will find out during their inspection anyway, and then you’ve wasted everyone’s time.

Can I negotiate a higher price with a cash buyer?

Absolutely, but your success depends on understanding what cards you’re holding. Cash buyers aren’t rigid – they’re running businesses, and like any business, they want to close deals.

Your negotiating power comes down to a few key factors. In hot markets with limited inventory, buyers compete more aggressively for properties. If your home is in a great neighborhood or has unique features that make it especially desirable, you’ve got leverage.

The magic happens when you have multiple offers. Even if all the cash offers are below market value, there can be significant differences between them. One buyer might offer $180,000 while another offers $195,000 for the same property.

Here’s a pro tip: being flexible on terms can sometimes get you more money. If a buyer really wants your property but their initial offer is at their maximum, they might pay more if you can close in 10 days instead of 30, or if you’re flexible about leaving certain appliances.

But let’s be honest about the limits. Cash buyers have maximum prices they can pay and still make their business model work. They need room for repairs, holding costs, and profit. If you absolutely need top dollar and have time to wait, a traditional sale with financing might serve you better.

The key is understanding what matters most to you – speed and convenience, or maximum price. There’s no wrong answer, just different priorities for different situations.

The Real Value of Working With Buy Homes Fast Cash Experts Like Greenlight Offer

Selling your home for cash isn’t just about getting money quickly – it’s about finding peace of mind when life throws you a curveball. Whether you’re staring down foreclosure papers, dealing with a divorce, or trying to figure out what to do with an inherited property that’s three states away, buy homes fast cash companies can offer a lifeline when traditional real estate feels impossible.

The truth is, cash sales aren’t perfect for everyone. You’ll probably get less money than if you fixed everything up and listed with an agent. But here’s what you won’t get: months of stress, surprise repair bills, deals falling through at the last minute, or strangers traipsing through your home every weekend.

After helping thousands of Houston families through these decisions, I’ve learned that the “best” choice isn’t always about maximizing every dollar. Sometimes it’s about getting certainty when everything else feels uncertain. Sometimes it’s about stopping the financial bleeding when holding costs are eating you alive. And sometimes it’s simply about moving on with your life instead of being tied to a property that’s become a burden.

The key is working with someone you can trust. A legitimate cash buyer will never rush you, will always show you proof they actually have the money, and will answer every question you have – even the ones you ask three times because you’re stressed and can’t remember the answer.

At Greenlight Offer, we’ve seen it all. The single mom in Humble facing foreclosure who got to keep her kids in the same school district because we closed in 14 days. The siblings in Sugar Land who couldn’t agree on what to do with their parents’ house until we bought it as-is and let them split the proceeds fairly. The landlord in The Woodlands who was just tired of dealing with problem tenants and wanted out.

Every situation is different, but the relief on people’s faces when they realize there’s a solution? That never gets old.

If you’re considering selling for cash, take your time to understand your options. Get multiple offers, ask lots of questions, and don’t let anyone pressure you into signing anything until you’re completely comfortable. The right buyer will respect your timeline and give you space to make the best decision for your family.

Most importantly, trust your gut. If something feels off, it probably is. If someone seems too pushy or won’t provide proof of funds, keep looking. There are plenty of legitimate cash buyers out there who will treat you fairly and with respect.

The cash home buying industry continues to grow because it solves real problems for real people. When traditional real estate isn’t working – whether because of timing, property condition, or personal circumstances – cash buyers provide an alternative that can genuinely help.

For more detailed information about how the entire process works and what to expect, check out our comprehensive guide on We Buy Houses for Cash. You’ll find everything you need to make an informed decision about whether selling for cash is right for your situation.

You’re not just selling a house – you’re solving a problem and moving forward with your life. The right cash buyer will understand that and work with you to make it happen as smoothly as possible.